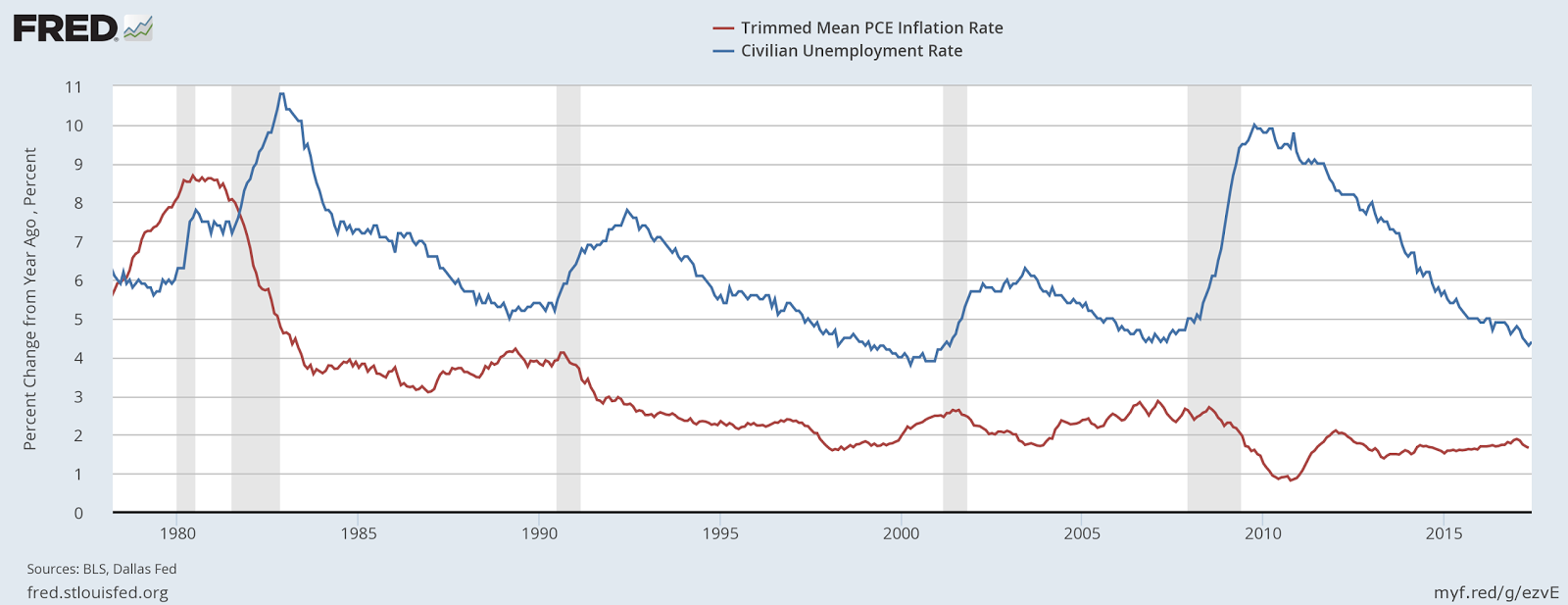

On December 17, 2015, the FOMC has raised its policy rate (IOER) from 25bp to 50bp. It has since raised the IOER rate three more times to 1.25%. Many on the committee seem convinced that further rate hikes are needed (in addition to actions designed to shrink the Fed's balance sheet, which is already shrinking relative to the size of the economy). What is the source of this enthusiasm for monetary policy tightening, given that the unemployment rate is close to target, and given a PCE inflation rate that has been undershooting the Fed's 2% inflation target for several years now?

The short answer is the Phillips curve. Or, to be more precise, a belief in the Phillips curve theory of inflation. The basic idea is that at very low rates of unemployment, competition for workers will lead to higher wages, with the associated costs passed on to consumers in the form of higher prices. Even if this wage pressure has been largely absent to date, it will (form sign of the cross here) eventually happen, and it's better for the Fed to get ahead of the curve, rather than risk having to raise its policy rate abruptly (and disruptively) in the future.

But what if the Phillips curve theory of inflation is not the best way to guide our thinking on the matter? What other theory might we turn to for guidance? Binyamin Appelbaum of the New York Times discusses a number of alternatives here (which I review in my previous post). In addition to the Phillips curve theory, he mentions explanations that I labeled: [1] Monetarist, [2] Expectations, [3] Internationalist/Technology. I mentioned in my previous post that I'd return to examining the Monetarist view, which I think is too often given a short shrift. I explain below how the Monetarist view is consistent with [2] and [3]. There is also the question of what the Monetarist view implies for policy. While the Phillips curve view has turned doves into hawks, I argue below that the Monetarist view should turn hawks into doves (given the present state of the economy).

Many people feel Monetarism has been discredited because economists who employed the theory to predict the inflationary consequences of QE were proved embarrassingly wrong. But this is along the lines of viewing scissors as a lousy tool because many barbers have used scissors to give awful haircuts.

To be fair to their critics, Monetarists sometimes overstate the role of money supply in determining the price-level and inflation. But let's also give credit where credit is due. We know how to create inflation. Just look at Venezuela today. No one can take seriously the notion that inflation is very high in Venezuela because the unemployment rate is far below its natural rate. Moreover, we know how to stop inflation. Tom Sargent's The Ends of Four Big Inflations showed us how it was done in history. Our understanding of these episodes revolve around Monetarist explanations that also take seriously fiscal considerations. Why can't the same theory be used to understand the present low-inflation environment and help guide policy? I think it can.

By the way, I've worked this all out in an open-economy version of the model I describe here. But nothing I say below hinges on this specific formalization; the basic idea is much more general. The two essential elements are: [1] safe government debt is a close substitute for central bank money; and [2] the demand for government money/debt can wax and wane over time (perhaps in St. Louis Fed regime-switching style).

The first property is important for understanding the economic consequences of open-market operations like QE. In the old days, when U.S. treasuries were yielding (say) 10% and Fed reserve liabilities were yielding 0%, an open-market swap of money for bonds could be expected to have a big effect. The same size open-market swap in a world of 1% reserves and 2% treasuries is not likely to have as great an impact. In the extreme case where reserves and treasuries have identical yields, open-market operations are not likely to have any effect at all--apart from inducing banks to accumulate excess reserves (in place of the treasuries they would have otherwise held). I think this is the main reason for why large-scale asset-purchase (LSAP) programs have had much smaller effects than what many had expected.

The fact that bonds become close substitutes for money when their yields are similar explains how the supply and demand for bonds can influence the inflation rate. Normally, we think of an increase in the demand for bonds as lowering bond yields. This is correct. But what happens when those yields approach the corresponding yield on interest-bearing money? (In the old days, when interest on reserves was zero, this limit was called the zero-lower-bound). An increase in the demand for bonds in this case must manifest itself in other ways. One way is for the price-level to fall. That is, a market-mechanism for expanding the real supply of nominal bonds is for the price-level to fall. One way this manifests itself is as China selling its goods for less USDs to acquire the USTs it so desperately wants.

The second property is important for understanding how inflation can fall even in the face of a growing supply of money/bonds. Admittedly, a bit of religion is required here, but I'm not sure what else to believe in. Suppose we can observe the supply of oil. We see a sudden increase in the supply of oil. At the same time, we see the price of oil rise. While the demand for oil is not directly observable, I think it's fair to say that most people would conclude that the (unobserved) demand for oil must have increased by more than the (observed) increase in supply. I want to apply the same thought-organizing principle to the price of money and bonds.

The story is familiar to those who point to declining money (and debt) velocity. In my formal model, I have a parameter that indexes the growth rate in the demand for real money/bond balances (where money and bonds take the form of USDs and USTs, respectively). In the open-economy version of my model, I have a "money demand growth regime" originating from the foreign sector. In the model, this regime translates into persistent U.S. trade deficits, representing the foreign sector's desire to acquire USD/UST at an elevated pace. There is in fact considerable evidence suggesting a large and growing foreign appetite for U.S. money/bonds over the past decade. Japan and China have each accumulated about one trillion dollars in USTs, for example. Moreover, it is known that USTs play an important role as exchange media (collateral) in credit derivatives markets and the shadow banking sector. Lately, the demand for such securities has been enhanced by a variety of regulatory reforms targeting the banking sector.

Bringing these elements together, the story that unfolds goes something like this. For years, several forces have conspired to elevate the (growth in the) demand for USD/USTs, driving yields ever lower. The financial crisis and associated "flight to quality" phenomenon served to exacerbate this secular force (with subsequent regulatory reforms adding to it further). Given an historically normal pace of money/debt expansion, these forces would have been hugely deflationary. The effect of the large increase in USTs following the crisis was to counteract this deflationary effect. But the U.S. debt-to-GDP ratio has essentially flat-lined since 2013. In the meantime, demand for the product continues to grow. With bond yields very close to the Fed's IOER rate, the result is persistently low inflation. And it's no surprise that now, after years of low inflation, that inflation expectations remain subdued.

No doubt some of you will find holes in this story, some inconsistencies perhaps, with past episodes or other countries. But I'm not claiming that this is the story; I'm simply suggesting that it may be an important part of it. And to the extent that it is, what does it imply about the current configuration of monetary and fiscal policy?

In my model, raising the policy rate in the face of stable or declining inflation has the effect of increasing the attractiveness of government money/bonds. The model highlights a portfolio substitution effect where savers redirect resources away from private capital spending (including expenditure on recruiting activities) toward money and bonds. The effect is contractionary. Is this really what we want/need right now? Moreover, in my model, the effect a higher policy rate on inflation depends critically on how the fiscal authority responds. (As Eric Leeper and others keep on reminding us, every monetary policy action must have a fiscal consequence.) A higher policy rate will increase the carrying cost of the debt, and Fed remittances to the U.S. treasury will decline. How will this added fiscal burden be financed? If the government makes no adjustment to its tax/spend policies, then the treasury will be forced to increase debt-issuance at a more rapid pace--an effect that is likely to increase the inflation rate (a result consistent with the so-called NeoFisherian view). Alternatively, if the government goes into austerity mode, cutting expenditures and/or raising taxes, the effect is likely to be disinflationary. This is all based on standard Monetarist thinking--we do not need the Phillips curve (which, by the way, exists in my model via a Tobin effect).

To the extent that the forces I've described above are present in reality, the analysis here calls into question the need for monetary policy tightening too rapidly at this time. Low unemployment does not necessarily portend higher inflation. And keep in mind that other measures of labor market activity, like the prime-age employment-to-population ratio, are still below their historical norms. Of course, this does not mean that monetary policy makers can afford to ignore the threat of inflation. While the worldwide demand for U.S. nominal debt instruments has been robust for a long time now, this "high U.S. money demand" regime is not likely to last forever. When the growth in money demand abates, the consequence is likely to manifest itself as higher inflation expectation (and bond yields)--much like what we observed following the November 2016 presidential election in the United States, except on a much larger scale. A good policy framework should make provisions for these and other contingencies, including sudden changes in the structure of fiscal policy.

Let me sum up and conclude. An elevated demand for U.S. dollars and treasuries has put downward pressure on bond yields and the inflation rate. Both the Fed and U.S. Treasury have partially accommodated this elevated demand. The result is a PCE inflation rate averaging about 1.5% since 2009, only 50bp below the Fed's official 2% target. The economic losses (or gains) associated with this "missing" 50bp of inflation going forward are difficult to quantify, but it's difficult for me to imagine that they are very large (and especially at this point in the recovery dynamic, where inflation expectations appear roughly consistent with the actual inflation rate).

But suppose that I am wrong and that it would be desirable to raise the price-level path back to its pre-2008 trend (something that would require a few years of inflation running above 2%). Is this even economically feasible? Does economic theory and experience provide a recipe? The answer is yes: have the central bank monetize the deficit until the price-level hits its target. (If the price-level never rises, then the government can enjoy a perpetual free lunch, cutting taxes and paying for goods and services with newly-issued non-inflationary money.)

But don't hold your breath for this to happen anytime soon. The constraints in place are not economic, they are political. Many public officials and the people they represent are growing uncomfortable with historically high debt-to-GDP ratios and large central bank balance sheets. They see the large supply of government debt, but they cannot see the large demand for the product driving yields down. Instead, they interpret low interest rates as enabling a large supply. And so, political pressure is presently running in the direction of austerity and smaller central bank balance sheets. Of course, if this is what the people want, this is what the people should get. But then, let's not spend so much time fretting over a 50bp miss on inflation, or bemoan the apparent lack of a coherent theory of inflation.

*******

PS. This post was motivated in part by Noah Smith, who tweeted:

I discuss the case of Japan in greater detail here: The failure to inflate Japan

The short answer is the Phillips curve. Or, to be more precise, a belief in the Phillips curve theory of inflation. The basic idea is that at very low rates of unemployment, competition for workers will lead to higher wages, with the associated costs passed on to consumers in the form of higher prices. Even if this wage pressure has been largely absent to date, it will (form sign of the cross here) eventually happen, and it's better for the Fed to get ahead of the curve, rather than risk having to raise its policy rate abruptly (and disruptively) in the future.

But what if the Phillips curve theory of inflation is not the best way to guide our thinking on the matter? What other theory might we turn to for guidance? Binyamin Appelbaum of the New York Times discusses a number of alternatives here (which I review in my previous post). In addition to the Phillips curve theory, he mentions explanations that I labeled: [1] Monetarist, [2] Expectations, [3] Internationalist/Technology. I mentioned in my previous post that I'd return to examining the Monetarist view, which I think is too often given a short shrift. I explain below how the Monetarist view is consistent with [2] and [3]. There is also the question of what the Monetarist view implies for policy. While the Phillips curve view has turned doves into hawks, I argue below that the Monetarist view should turn hawks into doves (given the present state of the economy).

Many people feel Monetarism has been discredited because economists who employed the theory to predict the inflationary consequences of QE were proved embarrassingly wrong. But this is along the lines of viewing scissors as a lousy tool because many barbers have used scissors to give awful haircuts.

To be fair to their critics, Monetarists sometimes overstate the role of money supply in determining the price-level and inflation. But let's also give credit where credit is due. We know how to create inflation. Just look at Venezuela today. No one can take seriously the notion that inflation is very high in Venezuela because the unemployment rate is far below its natural rate. Moreover, we know how to stop inflation. Tom Sargent's The Ends of Four Big Inflations showed us how it was done in history. Our understanding of these episodes revolve around Monetarist explanations that also take seriously fiscal considerations. Why can't the same theory be used to understand the present low-inflation environment and help guide policy? I think it can.

By the way, I've worked this all out in an open-economy version of the model I describe here. But nothing I say below hinges on this specific formalization; the basic idea is much more general. The two essential elements are: [1] safe government debt is a close substitute for central bank money; and [2] the demand for government money/debt can wax and wane over time (perhaps in St. Louis Fed regime-switching style).

The first property is important for understanding the economic consequences of open-market operations like QE. In the old days, when U.S. treasuries were yielding (say) 10% and Fed reserve liabilities were yielding 0%, an open-market swap of money for bonds could be expected to have a big effect. The same size open-market swap in a world of 1% reserves and 2% treasuries is not likely to have as great an impact. In the extreme case where reserves and treasuries have identical yields, open-market operations are not likely to have any effect at all--apart from inducing banks to accumulate excess reserves (in place of the treasuries they would have otherwise held). I think this is the main reason for why large-scale asset-purchase (LSAP) programs have had much smaller effects than what many had expected.

The fact that bonds become close substitutes for money when their yields are similar explains how the supply and demand for bonds can influence the inflation rate. Normally, we think of an increase in the demand for bonds as lowering bond yields. This is correct. But what happens when those yields approach the corresponding yield on interest-bearing money? (In the old days, when interest on reserves was zero, this limit was called the zero-lower-bound). An increase in the demand for bonds in this case must manifest itself in other ways. One way is for the price-level to fall. That is, a market-mechanism for expanding the real supply of nominal bonds is for the price-level to fall. One way this manifests itself is as China selling its goods for less USDs to acquire the USTs it so desperately wants.

The second property is important for understanding how inflation can fall even in the face of a growing supply of money/bonds. Admittedly, a bit of religion is required here, but I'm not sure what else to believe in. Suppose we can observe the supply of oil. We see a sudden increase in the supply of oil. At the same time, we see the price of oil rise. While the demand for oil is not directly observable, I think it's fair to say that most people would conclude that the (unobserved) demand for oil must have increased by more than the (observed) increase in supply. I want to apply the same thought-organizing principle to the price of money and bonds.

The story is familiar to those who point to declining money (and debt) velocity. In my formal model, I have a parameter that indexes the growth rate in the demand for real money/bond balances (where money and bonds take the form of USDs and USTs, respectively). In the open-economy version of my model, I have a "money demand growth regime" originating from the foreign sector. In the model, this regime translates into persistent U.S. trade deficits, representing the foreign sector's desire to acquire USD/UST at an elevated pace. There is in fact considerable evidence suggesting a large and growing foreign appetite for U.S. money/bonds over the past decade. Japan and China have each accumulated about one trillion dollars in USTs, for example. Moreover, it is known that USTs play an important role as exchange media (collateral) in credit derivatives markets and the shadow banking sector. Lately, the demand for such securities has been enhanced by a variety of regulatory reforms targeting the banking sector.

Bringing these elements together, the story that unfolds goes something like this. For years, several forces have conspired to elevate the (growth in the) demand for USD/USTs, driving yields ever lower. The financial crisis and associated "flight to quality" phenomenon served to exacerbate this secular force (with subsequent regulatory reforms adding to it further). Given an historically normal pace of money/debt expansion, these forces would have been hugely deflationary. The effect of the large increase in USTs following the crisis was to counteract this deflationary effect. But the U.S. debt-to-GDP ratio has essentially flat-lined since 2013. In the meantime, demand for the product continues to grow. With bond yields very close to the Fed's IOER rate, the result is persistently low inflation. And it's no surprise that now, after years of low inflation, that inflation expectations remain subdued.

No doubt some of you will find holes in this story, some inconsistencies perhaps, with past episodes or other countries. But I'm not claiming that this is the story; I'm simply suggesting that it may be an important part of it. And to the extent that it is, what does it imply about the current configuration of monetary and fiscal policy?

In my model, raising the policy rate in the face of stable or declining inflation has the effect of increasing the attractiveness of government money/bonds. The model highlights a portfolio substitution effect where savers redirect resources away from private capital spending (including expenditure on recruiting activities) toward money and bonds. The effect is contractionary. Is this really what we want/need right now? Moreover, in my model, the effect a higher policy rate on inflation depends critically on how the fiscal authority responds. (As Eric Leeper and others keep on reminding us, every monetary policy action must have a fiscal consequence.) A higher policy rate will increase the carrying cost of the debt, and Fed remittances to the U.S. treasury will decline. How will this added fiscal burden be financed? If the government makes no adjustment to its tax/spend policies, then the treasury will be forced to increase debt-issuance at a more rapid pace--an effect that is likely to increase the inflation rate (a result consistent with the so-called NeoFisherian view). Alternatively, if the government goes into austerity mode, cutting expenditures and/or raising taxes, the effect is likely to be disinflationary. This is all based on standard Monetarist thinking--we do not need the Phillips curve (which, by the way, exists in my model via a Tobin effect).

To the extent that the forces I've described above are present in reality, the analysis here calls into question the need for monetary policy tightening too rapidly at this time. Low unemployment does not necessarily portend higher inflation. And keep in mind that other measures of labor market activity, like the prime-age employment-to-population ratio, are still below their historical norms. Of course, this does not mean that monetary policy makers can afford to ignore the threat of inflation. While the worldwide demand for U.S. nominal debt instruments has been robust for a long time now, this "high U.S. money demand" regime is not likely to last forever. When the growth in money demand abates, the consequence is likely to manifest itself as higher inflation expectation (and bond yields)--much like what we observed following the November 2016 presidential election in the United States, except on a much larger scale. A good policy framework should make provisions for these and other contingencies, including sudden changes in the structure of fiscal policy.

Let me sum up and conclude. An elevated demand for U.S. dollars and treasuries has put downward pressure on bond yields and the inflation rate. Both the Fed and U.S. Treasury have partially accommodated this elevated demand. The result is a PCE inflation rate averaging about 1.5% since 2009, only 50bp below the Fed's official 2% target. The economic losses (or gains) associated with this "missing" 50bp of inflation going forward are difficult to quantify, but it's difficult for me to imagine that they are very large (and especially at this point in the recovery dynamic, where inflation expectations appear roughly consistent with the actual inflation rate).

But suppose that I am wrong and that it would be desirable to raise the price-level path back to its pre-2008 trend (something that would require a few years of inflation running above 2%). Is this even economically feasible? Does economic theory and experience provide a recipe? The answer is yes: have the central bank monetize the deficit until the price-level hits its target. (If the price-level never rises, then the government can enjoy a perpetual free lunch, cutting taxes and paying for goods and services with newly-issued non-inflationary money.)

But don't hold your breath for this to happen anytime soon. The constraints in place are not economic, they are political. Many public officials and the people they represent are growing uncomfortable with historically high debt-to-GDP ratios and large central bank balance sheets. They see the large supply of government debt, but they cannot see the large demand for the product driving yields down. Instead, they interpret low interest rates as enabling a large supply. And so, political pressure is presently running in the direction of austerity and smaller central bank balance sheets. Of course, if this is what the people want, this is what the people should get. But then, let's not spend so much time fretting over a 50bp miss on inflation, or bemoan the apparent lack of a coherent theory of inflation.

*******

PS. This post was motivated in part by Noah Smith, who tweeted:

Conclusion:— Noah Smith (@Noahpinion) August 4, 2017

NO ONE KNOWS HOW INFLATION WORKS.

Macroeconomists need to go back to the drawing board on inflation. Square one.

I discuss the case of Japan in greater detail here: The failure to inflate Japan